The income chargeable under the head "Salaries" is registered after making the following deductions under Section 16:

1. Standard Deduction;

2. Entertainment Allowance Deduction; and

3. Professional Tax.

1. Standard Deduction [Sec. 16(i)/(ia)] -

• Standard deduction is Rs. 50,000; or

• the Amount of Salary,

Whichever is lower.

2. Entertainment Allowance [Sec. 16(ii)]-

Entertainment allowance may consider if the below conditions:-

(A). In the case of an Administration representative (i.e., a Central Government or a State Government worker), the least of the following is Deductible:

a. Rs. 5,000;

b. 20 % of Basic Salary; or

c. Amount of Entertainment Allowance granted during the earlier year.

In request to determine the amount of entertainment allowance deductible from salary, the following points need consideration:

1. For this reason "salary" avoids any allowance, advantage or other perquisites.

2. Amount actually used towards entertainment (out of entertainment allowance got) is not taken into consideration.

(B). In the case of a Non-Government Representative (including workers of Statutory Corporation and Local Authority), :

Entertainment Allowance is NOT deductible.

3. Professional Tax or Tax on Work [Sec. 16(iii)] -

Professional Tax or Tax on Work, collected by a State under article 276 of the Constitution, is allowed as Deduction.

The following points ought to be kept in see:-

1. Deduction is available just in the year in which professional tax is paid.

2. If the professional tax is paid by the business on behalf of a representative, it is first included in the salary of the worker as a "perquisite" and then the same amount is allowed as a deduction on account of "professional tax" from net salary.

3. If there is no monetary ceiling under the Income-tax Act. Under article 276 of the Constitution, a State Government cannot force more than Rs. 2,500 for each annum as professional tax. Under the Income-tax Act, whatever professional tax is paid during the earlier year, is deductible.

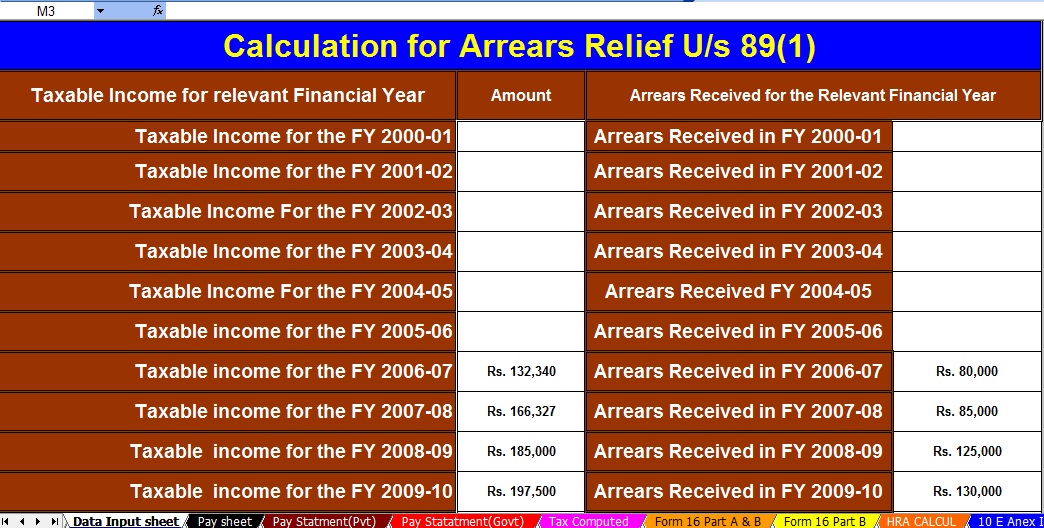

Download Automated Income Tax Arrears Relief Calculator U/s 89(1) along with Form 10Efrom the Financial Year 2000-01 to Financial Year 2020-21 (Up-to-date Version)

0 Comments