Taxes are an essential constituent in India. A major portion of the income incurred by the government is accounted for them. This income is the income that is used to offer certain basic provisions to the citizens. An individual is expected to make payment of taxes, according to the existing tax slabs, if he earns a certain amount. Though these taxes could be harsh on the taxpayer’s bank balance, the government also offers certain provisions through which one can save taxes. Tax deductions assist you in reducing the taxable income by lowering the overall tax liability and thus aiding them on saving taxes. The ones who are eligible for deductions depend on several factors, with different limits fixed for different purposes.

Download Automated TDS on Salary All in One for Govt & Non- Govt employees for F.Y.2017-18 [ This Excel Utility can prepare at a time Tax Compute Sheet + Automatic Arrears Relief Calculator with Form 10E + Automated H.R.A. Calculation + Automated Form 16 Part A&B and Form 16 Part B as per the new Tax Slab for F.Y.2017-18]

Synopsis of Tax Deductions U/S 80 C to 80 U:

Section

|

Allowed Limit (Maximum)

|

Eligible Petitioner (Claimant)

|

80 C

|

Rs 1.5 lakh (cumulative of 80C, 80CCC and 80CCD)

|

Hindu Undivided Families/Individuals

|

80 CCC

|

Rs 1.5 lakh (cumulative of 80C, 80CCC and 80CCD)

|

Individuals

|

80 CCD

|

Rs 1.5 lakh (cumulative of 80C, 80CCC and 80CCD)

|

Individuals

|

80CCD(2)

|

10@of Salary ( Contribution to the employees Pension Fund )

|

Individuals

|

80 CCD(1B)

|

Rs. 50,000/- ( Additional deduction under Section 80C0

|

Individuals

|

80 D

|

Rs. 25, 000/- for below 60 years & Rs. 30,000/- for above 60 Years

|

Individuals

|

80 DD

|

Rs. 75, 000 (general disability)

Rs. 1. 25 lakhs (critical disability)

|

Individuals

|

80 DDB

|

Rs. 60, 000 (senior citizens)

Rs. 40, 000 (others)

|

Individuals

|

80 E

|

No limit specified (Educational Loan Interest)

|

Individuals

|

80 EE

|

Rs. 50,000/-

|

Individuals

|

80 G

|

Different limits depending on donation

|

All assessee

|

80 GG

|

Rs. 5, 000/- per month

|

Individuals who do not receive HRA

|

80 TTA

|

Rs. 10, 000 per year

|

Hindu Undivided Families/ Individuals

|

80 U

|

Rs. 75, 000 (People with disabilities)

Rs. 1.25 lakhs (people with critical disabilities)

|

Resident Individuals

|

87 A

|

Tax Rebate Rs.2,500/- who’s Taxable Income below Rs 3.5 Lakh

|

Resident Individuals

|

What is Tax Deduction?

Tax deduction assists in trimming down your income subject to tax. It reduces the overall tax liabilities and aids you save tax. However, the amount of deduction differs depending on the kind of tax deduction claimed by you. A tax deduction can be claimed for the amounts spent in medical expenses, tuition fees and charitable contributions. Also, you can make an investment in several schemes like retirement saving schemes, life insurance plans and national saving schemes etc. The Indian Government provides tax exemptions for several expenses that are incurred in various activities to stimulate commercial institutions and the individuals to participate in activities having social benefits.

Many of our day-to-day expenses qualify for deductions, along with the information about them being vital to assist us in saving money. You can claim the tax deduction on money spent for medical expenses, education, retirement schemes, investments in insurance, charitable contributions etc. These deductions are practiced to stimulate society members to take part in certain helpful activities, aiding everyone drawn in the process.

Download Automated Income Tax preparation Excel Based Software for Non-Govt employees for F.Y.2017-18 [ This Excel Utility can prepare at a time Tax Compute Sheet + Automated H.R.A. Exemption Calculation + Automated Form 12 BA + Automated Form 16 Part A&B and Form 16 Part B for F.Y.2017-18]

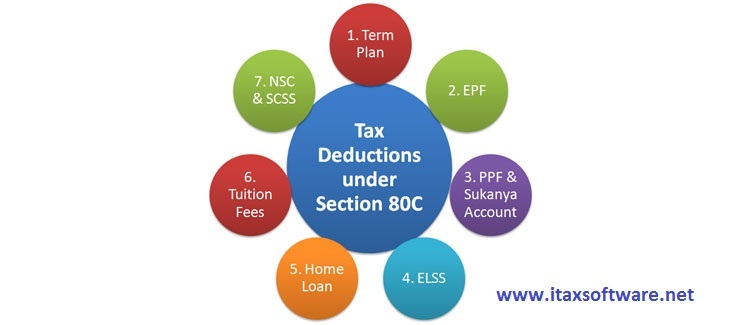

Income Tax Deductions under Section 80C:

Income Tax Act’s Section 80C offers provisions for income tax rebate on several payments, with Hindu Undivided Families and individuals eligible for such deductions. The individuals who are eligible to pay taxes can claim deductions up to Rs. 1.5 lakh per year as per section 80C, with this sum being a combo of deductions applicable under Sections 80C, 80CCC and 80CCD.

A few of the prominent investments that are eligible for the tax rebate are:

- Life Insurance Policies payments (for spouse, self or children)

- Superannuation/provident fund payments

- Payment made towards tuition fees to educate maximum two children

- Payments for construction or buying of a residential property

- Payments made towards a fixed deposit of minimum tenure of 5 years

The Section 80C of the IT Act 1961 offers several additional deductions such as mutual funds investment, buying NABARD bonds, senior citizens savings schemes etc.

Download Automated Income Tax Preparation Excel Based Software for West Bengal Govt Employees for F.Y.2017-18 [ This Excel Utility Can prepare at a time your Tax Compute Sheet +Automated H.R.A. Exemption Calculation + Individual Salary Structure + Automated Form 16 Part A&B and Form 16 Part B for F.Y.2017-18 ]

Subsections under Section 80C:

There is an exhaustive list of deductions under Section 80C of the Income Tax Act, 1961.

Section 80 CCC:

This section of the IT Act, 1961 offers a purview for tax rebates on investments made in the pension funds. Any insurer can offer these pension funds and can claim a maximum deduction of Rs. 1.5 lakh under it. Only individual taxpayers can claim this deduction.

Section 80 CCD:

The Income Tax Act’s Section 80 CCD intends to boost the saving habits among people offering them an incentive for making an investment in pension plans that are declared by the Central Government of India. Both the contributions made by an individual and his employer are eligible for tax deduction, liable to be subjected to the deduction of less than 10% of the person’s salary.

Download Automated Arrears Relief Calculator U/s 89(1) with Form 10E from F.Y. 2000-01 to 2017-18 ( Up dated Version)

Income Tax Rebate Under Section 80D:

Income Tax Act’s Section 80D allows deductions on the amounts spent towards the health insurance policy’s premiums by an individual. This takes payments made on behalf of parents, spouse, children or self to a health plan by Central Government. You can claim a sum of Rs. 25, 000 as a deduction when making a payment towards the insurance for your spouse, self or dependent children, while this sum is Rs. 30, 000 if an individual is over 60 years of age.

Both Hindu Undivided Families and individuals are eligible for the deduction under this section, depending on the mode of payment other than cash.

Section 80DD:

Section 80DD of the Income Tax Act offers provisions for tax deductions in two situations, with the deduction of Rs. 1.5 lakh in case of a severe disability and Rs. 75, 000 in the case of normal disability. You can claim the deduction under this section in the case of the expenditures below:

- On making payments for the treatment of the dependents with disability

- Payment of amount made as a premium to maintain or buy an insurance policy for these dependents.

A deduction of Rs. 1.25 lakh for a critical disability and Rs. 75, 000 for normal disability is allowed. Both resident individuals and Hindu Undivided Families are eligible for such deduction. In this case, the dependent can either be parents, spouse, children or siblings.

Download All in One TDS on Salary for Central & State Govt employees for the F.Y.2017-18

Section 80DDB:

Section 80DDB of The Income Tax Act can be used by resident individuals and HUFs and offers provisions for deductions on the expenditure incurred by family/an individual towards medical treatment of a particular disease. A deduction of Rs. 40, 000 that can be increased up to Rs. 60, 000, is allowed if treatment for senior citizens.

Tax Deductions Under Section 80 E:

Section 80 E of the IT Act 1961 is designed to make sure that educating an individual does not become an added tax burden. Tax payers are qualified for tax deductions to pursue higher education on the interest repayment of a loan. You can avail this loan either by the taxpayer himself or to fund his child/ward’s education. Only individuals, who have taken loans from any approved financial institutions and charitable organisations, are allowed for tax benefits.

Subsections of Section 80 E:

Section 80EE:

Only individual taxpayers qualify for deductions under this section, with the interest repayment of a loan, which the individual has taken to purchase a residential property being eligible for deductions. Under this section, you can avail a maximum deduction of Rs. 3 lakh.

Tax Deductions under Section 80 G:

Section 80G of the Income Tax Act allows the taxpayers to contribute funds to charitable institutions, providing them with tax benefits on fiscal donations. This deduction can be availed by all assessee, subject to them offering a proof of payment, with the deductions’ limit decided depending on some factors.

1) 100% deductions without any limit:

100% deductions are provided on the donations to funds such as Prime Minister’s Relief Fund, National Defence Fund, and National Illness Assistance Fund etc.

2) 100% deduction with qualifying limit:

3) Contributions made towards local associations, authorities or institutes to endorse the growth of sports and family planning are eligible for 100% deductions, contingent to a certain qualifying limit.

50% deduction with qualifying limits:

Donations made towards the religious organisation and local authorities for reasons except family planning institutes and other charitable institutes qualify for 50% deductions, subject to a certain qualifying limit.

The qualifying limit is referred to 10% of tax payer’s gross total income.

Subsections of Section 80G:

Section 80G of the Income Tax Act, 1961 has been further subdivided into the following four categories to simplify understanding:

Section 80GG:

Those individual taxpayers, by whom the house rent allowance is not received, qualify for this deduction on the rent they pay, subject to the highest deduction equal to 25% of the total income incurred or Rs. 5, 000/- per month. You can claim the lower one out of these options as a deduction.

Section 80TTA:- Exemption from Savings Bank Interest Max Rs. 10,000/-

Section 87A :- Tax Rebate Rs.2,500/- who’s Taxable Income less than 3.5 Lakh.