Download and prepare at a time Tax Compute Sheet + Individual Salary Sheet + Individual Salary Structure as per Govt & Non-Govt employees Salary Pattern + Automated H.R.A. Exemption Calculation + Automatic Arrears Relief Calculation with Form 10E + Automated Form 16 Part A&B and Form 16 Part B for F.Y.2016-17

|

| Main Data Input Sheet for Deductor |

|

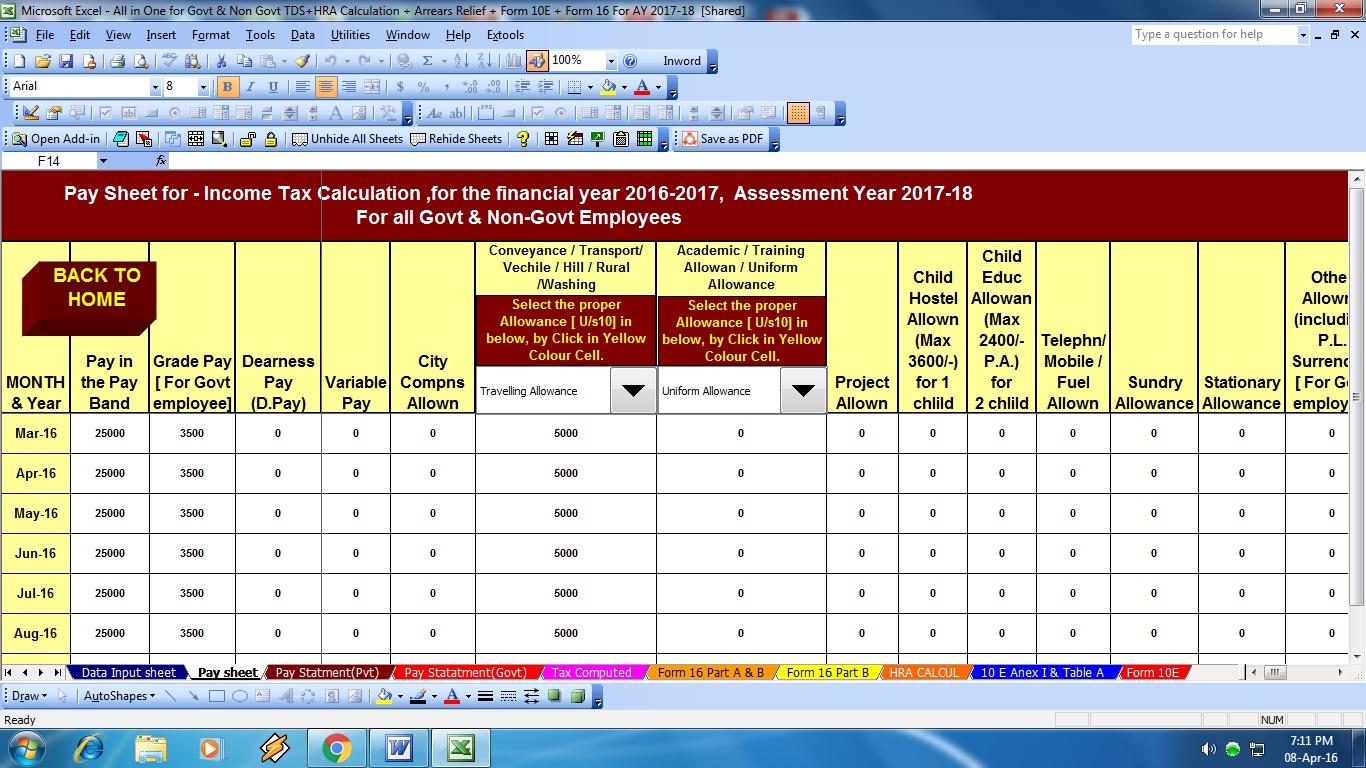

| Employees Salary Structure |

|

| Form 16 Part A&B |

|

| Form 16 Part B |

|

| Arrears Relief Calculator with Form 10E |

At the investment stage, National Pension System (NPS) offers the income tax benefits under different sections of the Income Tax Act – Section 80CCD (1), Section 80CCD (1b) and Section 80CCD (2).

NPS is especially useful for investors who may have exhausted the Rs 1.5 lakh investment limit under Section 80C but want to save more.

Under Section 80CCD (1) – Investment up to Rs 1.5 lakh into NPS in a financial year is eligible for deduction under Section 80CCD(1). This deduction comes under the overall ceiling of Rs 1.5 lakh for deduction under Section 80C.

Under Section 80CCD (1b) – In budget 2016, the government had introduced additional tax benefit for investment up to Rs 50,000 in NPS. If the taxpayer contributes more than Rs 1.5 lakh to the NPS in a year, the amount in excess of Rs 1.5 lakh can be claimed as a deduction under the new Section 80CCD(1b).

Under Section 80CCD(2): Over and above the ceiling limit of Rs 1.5 lakh provided under Section 80C and limit of Rs 50,000 under Section 80CCD(1B), contribution from the employer up to 10% of Basic Salary + Dearness Allowance is also eligible for deduction under Section 80CCD(2). There is no upper cap (in terms of amount) on this tax deduction and it is available only to employees.